SMM News on June 14:

Metal Market:

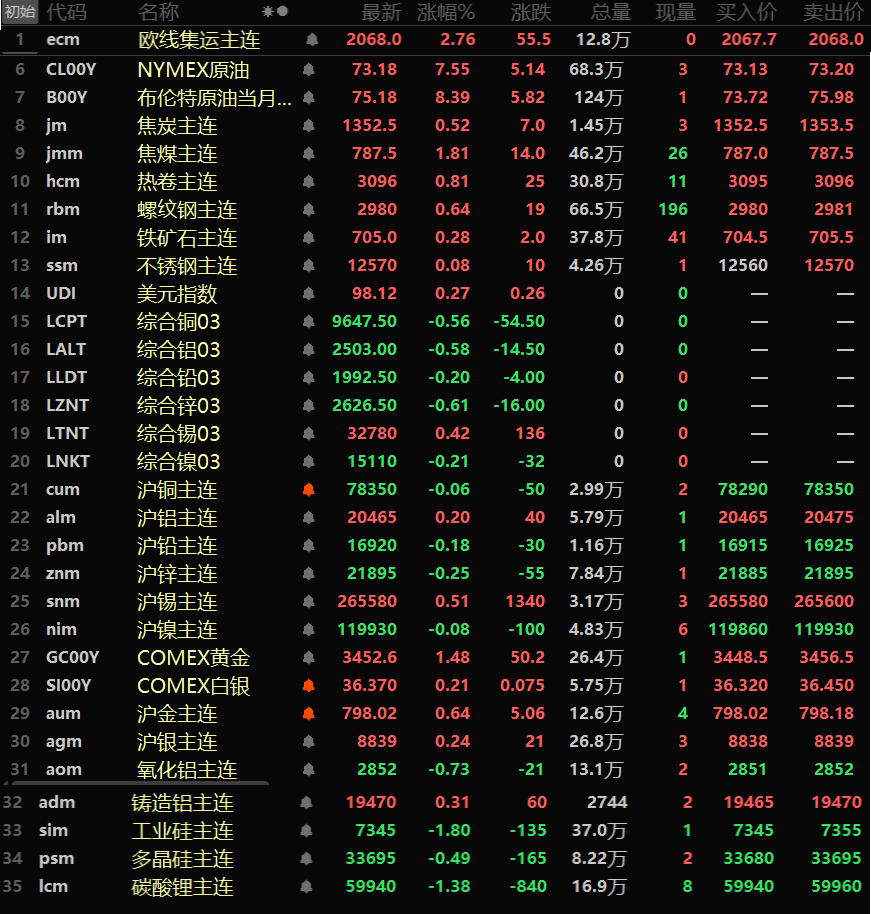

As of the overnight close, base metals in both domestic and overseas markets generally declined, with only LME tin, SHFE aluminum, and SHFE tin rising. LME tin rose 0.42%, SHFE aluminum rose 0.2%, and SHFE tin rose 0.51%. The rest of the metals fell, with LME copper down 0.56%, LME aluminum down 0.58%, and LME zinc down 0.61%. The declines in other metals were relatively minor. The main alumina contract fell 0.73%, while the main aluminum casting contract rose 0.31%.

The ferrous metals series generally rose, with rebar up 0.64% and HRC up 0.81%. In the coking coal and coke sector, coking coal rose 1.81% and coke rose 0.52%.

In precious metals, as of the overnight close, COMEX gold rose 1.48%, recording a three-day winning streak and hitting a new high since April 22, with a weekly gain of 3.17%. COMEX silver rose 0.21%, with a weekly gain of 0.64%. Domestically, SHFE gold rose 0.64%, with a weekly gain of 1.72%, and SHFE silver rose 0.24%, with a weekly gain of 0.42%.

As of 9:13 a.m. on June 14, Friday's overnight market close

》Click to view SMM Futures Data Dashboard

Macro Front

Domestic Aspects:

[PBOC: Social financing increased by 18.63 trillion yuan, new loans increased by 10.68 trillion yuan from January to May, M2 grew 7.9% YoY in May] According to preliminary statistics from the People's Bank of China (PBOC), China's social financing scale increased by 18.63 trillion yuan from January to May, compared to 16.3429 trillion yuan from January to April. New RMB loans increased by 10.68 trillion yuan from January to May, compared to 10.0597 trillion yuan from January to April. At the end of May, the balance of broad money (M2) was 325.78 trillion yuan, up 7.9% YoY. The balance of narrow money (M1) was 108.91 trillion yuan, up 2.3% YoY. The balance of currency in circulation (M0) was 13.13 trillion yuan, up 12.1% YoY. Net cash injection in the first five months was 306.4 billion yuan. 》Click to view details

The PBOC announced that to maintain ample liquidity in the banking system, on June 16, 2025, the People's Bank of China will conduct 400 billion yuan of outright reverse repo operations through fixed-quantity, interest-rate tenders with multiple-price awards, with a term of six months (182 days).

US Dollar Aspects:

The overnight US dollar index rose 0.27% to 98.12, with a weekly decline of 1.11%. Investors largely ignored data showing that US consumer confidence rebounded in June for the first time in six months. Data released by the University of Michigan's consumer survey on Friday showed that the consumer sentiment index jumped to 60.5 this month, higher than market expectations. Next week, the US Fed's FOMC will announce its interest rate decision and Summary of Economic Projections.

Other currencies:

In afternoon trading, the US dollar rose 0.3% against the Japanese yen to 143.88 yen and 0.1% against the Swiss franc to 0.8110 francs.

The US dollar fell against the Swiss franc for the second consecutive week. The euro fell 0.4% against the US dollar to $1.1539.

Data releases:

Next week, China will release data including the operation scale of the medium-term lending facility (MLF) on June 16, the winning bid rate of the MLF on June 16, the year-to-date annual rate of urban fixed asset investment in May, the year-to-date annual rate of industrial added value above designated size in May, the monthly annual rate of industrial added value above designated size in May, the annual rate of total retail sales of consumer goods in May, the year-to-date annual rate of total retail sales of consumer goods in May, the monthly rate of total retail sales of consumer goods in May, the monthly annual rate of total electricity consumption in May, the monthly total electricity consumption in May (irregularly from the 15th to the 20th), the one-year loan prime rate (LPR) in June, the five-year loan prime rate (LPR) in June, etc. The US will release data including the upper and lower limits of the target federal funds rate in June, the New York Fed manufacturing index in June, the New York Fed manufacturing index for the next six months' expectations in June, the monthly import price index in May, the annual rate of the import price index in May, the monthly rate of retail sales in May, the monthly rate of core retail sales in May, the annual rate of retail sales in May, the monthly rate of the retail sales control group associated with GDP in May (seasonally adjusted), the monthly rate of industrial output in May, the capacity utilisation rate in May, the monthly rate of manufacturing output in May, the manufacturing capacity utilisation rate in May, the annual rate of industrial output in May (seasonally adjusted), the initial annualized total of building permits in May, the initial jobless claims for the week ending June 14, the Philadelphia Fed manufacturing index in June, etc. The eurozone will release data including the total reserve assets in May, the ZEW economic sentiment index in June, the final unadjusted annual rate of core harmonized CPI in May, and the initial consumer confidence index in June. Japan will release data including the Bank of Japan's policy benchmark interest rate on June 17 (%)(irregularly on June 17), the unadjusted merchandise trade balance in May, the seasonally adjusted merchandise trade balance in May, the unadjusted merchandise exports in May, and the annual rate of the nationwide core CPI in May. The UK will release data including the annual rate of core CPI in May, the annual rate of the retail price index in May, the Bank of England's benchmark interest rate in June, the Gfk consumer confidence index in June, and the seasonally adjusted monthly rate of core retail sales in May. Australia will release data including the ANZ consumer confidence index for the week ending June 15, the seasonally adjusted unemployment rate in May, and the change in employed population in May. Data such as the quarterly rate of GDP in Q1 for New Zealand (production method, seasonally adjusted), the annual rate of GDP in Q1 for New Zealand (production method, seasonally adjusted), the monthly rate of core retail sales in April for Canada, the ZEW economic sentiment index in June for Germany, and the Bank of Switzerland's policy interest rate in June will also be released.

Additionally, the National Bureau of Statistics (NBS) will release the monthly report on residential sales prices in 70 large and medium-sized cities, and the State Council Information Office will hold a press conference on the national economic performance. On June 17, China has 182 billion yuan of 1-year medium-term lending facility (MLF) maturing. The Federal Open Market Committee (FOMC) of the US Fed will announce the interest rate decision and the Summary of Economic Projections, and Fed Chairman Powell will hold a press conference on monetary policy. US President Trump will visit Canada from June 15 to 17 to attend the G7 Leaders' Summit. The Swiss National Bank will announce its interest rate decision, and the Bank of England will also announce its interest rate decision. Kazuo Ueda, Governor of the Bank of Japan, will hold a press conference on monetary policy, and the Bank of Japan will announce its interest rate decision. The Bank of Canada will release the minutes of its monetary policy meeting, and Kazuo Ueda, Governor of the Bank of Japan, will deliver a speech.

Crude oil market:

Oil prices in both markets surged overnight, with US crude oil rising 7.55%, hitting a high of $77.62 per barrel during the session, a new high since January 20, and Brent crude oil rising 8.39%, reaching a high of $78.5 per barrel during the session, a new high since January 23. The escalation of regional tensions has sparked investor concerns about potential widespread disruptions to oil exports in the Middle East. Both benchmark crude oils recorded their largest intraday fluctuations since the energy price surge triggered by the Russia-Ukraine conflict in 2022.

The Iraqi National News Agency stated that Iraq has sufficient strategic reserves of key materials to prepare for the escalation of the situation in the region. The National Iranian Oil Refining and Distribution Company said that oil refining and storage facilities were undamaged and continued to operate. Iran, a member of the Organization of the Petroleum Exporting Countries (OPEC), currently has a daily production of about 3.3 million barrels, with oil and fuel exports exceeding 2 million barrels per day. According to analysts and OPEC observers, the spare capacity of OPEC and its allies (including Russia) to produce more oil to offset any disruptions is roughly equivalent to Iran's production.

Analysts and OPEC observers said that the rapid surge in oil prices is partly due to the fact that the spare capacity of OPEC and its allies to increase production to offset supply disruptions is roughly equivalent to Iran's production.

In other market news, US energy services company Baker Hughes stated in its closely watched report that the number of oil and natural gas rigs operated by US energy companies fell for the seventh consecutive week this week to the lowest level since November 2021. Data showed that as of the week ending June 13, the total number of US oil and natural gas rigs, a leading indicator of future production, decreased by 4 to 555, down 35 or 6% from the same period last year. (Wenhua Comprehensive)